Solution Methods for Microeconomic

Dynamic Stochastic Optimization Problems

2026-03-11

Christopher D. Carroll1

Note: The GitHub repo SolvingMicroDSOPsassociated with this document contains python code thatproduces all results, from scratch, except for the last section on indirect inference. The numerical results havebeen confirmed by showing that the answers that the raw python produces correspond to the answersproduced by tools available in the Econ-ARKtoolkit, more specifically those in the HARKwhichhas full documentation. The MSM results at the end have have been superseded by tools in theEstimatingMicroDSOPs repo.

Abstract These notes describe tools for solving microeconomic dynamic stochastic optimization problems,and show how to use those tools for efficiently estimating a standard life cycle consumption/savingmodel using microeconomic data. No attempt is made at a systematic overview of the many possibletechnical choices; instead, I present a specific set of methods that have proven useful in my own work(and explain why other popular methods, such as value function iteration, are a bad idea).Paired with these notes is Python code that solves the problems described in the text.

(Contains LaTeX code for this document and software producing figures and results)

1Carroll: Department of Economics, Johns Hopkins University, Baltimore, MD, ccarroll@jhu.eduThe notes were originally written for my Advanced Topics in Macroeconomic Theoryclass at Johns Hopkins University; instructors elsewhere are welcome to use them forteaching purposes. Relative to earlier drafts, this version incorporates several improvementsrelated to new results in the paper “Theoretical Foundations of Buffer Stock Saving”(especially tools for approximating the consumption and value functions). Like the last majordraft, it also builds on material in “The Method of Endogenous Gridpoints for SolvingDynamic Stochastic Optimization Problems” published in Economics Letters, available athttp://www.econ2.jhu.edu/people/ccarroll/EndogenousArchive.zip, and by including samplecode for a method of simulated moments estimation of the life cycle model a la ? and Cagetti (?).Background derivations, notation, and related subjects are treated in my class notes for first year macro,available at http://www.econ2.jhu.edu/people/ccarroll/public/lecturenotes/consumption. Iam grateful to several generations of graduate students in helping me to refine these notes, to MarcChan for help in updating the text and software to be consistent with ?, to Kiichi Tokuoka for draftingthe section on structural estimation, to Damiano Sandri for exceptionally insightful help in revising andupdating the method of simulated moments estimation section, and to Weifeng Wu and Metin Uyanikfor revising to be consistent with the ‘method of moderation’ and other improvements. All errors aremy own. This document can be cited as ? in the references.

1 Introduction

These notes provide a gentle-as-possible introduction to a particular set of

solution tools for the canonical consumption-saving/portfolio allocation problem

for a consumer facing uninsurable idiosyncratic risk to nonfinancial income

(e.g., labor or transfer income), first without and then with optimal portfolio

choice,1

with detailed intuitive discussion of various mathematical and computational techniques that,

together, accelerate the solution by many orders of magnitude. The problem is solved with and

without liquidity constraints, and the infinite horizon solution is the limit of the finite horizon

solution. After the basic consumption/saving problem with a deterministic interest rate is

described and solved, an extension with portfolio choice between a riskless and a risky asset is

also solved. Finally, a simple example shows how to use these methods (via the statistical

‘method of simulated moments’ (MSM for short)) to estimate structural parameters

like the coefficient of relative risk aversion (a la Gourinchas and Parker (?) and

Cagetti (?)).

2 The Problem

The usual analysis of dynamic stochastic programming problems packs a great many events

(intertemporal choice, stochastic shocks, intertemporal returns, income growth, the taking of

expectations, time discounting, and more) into a complex decision in which the agent

makes an optimal choice simultaneously taking all these elements into account.

For the dissection here, we will be careful to break down everything that happens

into distinct operations so that each element can be scrutinized and understood in

isolation.

We are interested in the behavior of a consumer who begins period

with a

certain amount of ‘capital’

(1)

which immediately earns a return factor .

Simultaneously, the consumer receives noncapital income

, which is the product

of ‘permanent income’

and a transitory shock :

(2)

whose expectation is 1 (that is, before realization of the transitory shock, the consumer’s

expectation is that actual income will on average be equal to permanent income

).

The combination of the capital return and income defines the consumer’s ‘market resources’

(sometimes called ‘cash-on-hand,’ following ?):

(3)

available to be spent on consumption

for a consumer subject to a liquidity constraint that requires

(though we are not imposing such a constraint yet—see subsection 6.8). Finally we define

(4)

mnemonically as ‘assets-after-all-actions-are-accomplished.’

The consumer’s goal is to maximize discounted utility from consumption over the rest of a lifetime

ending at date :

(5)

(6)

Income evolves according to:

(7)

(8)

Equation (8) indicates that we are allowing for a predictable average profile of income growth over

the lifetime

(to capture typical career wage paths, pension arrangements,

etc).2

Finally, the utility function is of the Constant Relative Risk Aversion (CRRA) form,

.

It is well known that this problem can be rewritten in recursive (Bellman) form:

(9)

(10)

subject to the Dynamic Budget Constraint (DBC) defined by equation (3), and to the

dynamic process for income defined in (8) and to a transition equation that defines next

period’s initial capital as this period’s end-of-period assets:

(11)

3 Normalization

The single most powerful method for speeding the solution of such models is to redefine the

problem in a way that reduces the number of state variables (if at all possible). In the

consumption context, the obvious idea is to see whether the problem can be rewritten in

terms of the ratio of various variables to permanent noncapital (‘labor’) income

(henceforth for brevity, ‘permanent income.’)

In the last period of life ,

there is no future value,

(boldface

denotes the value function in levels; the nonbold normalized counterpart

is

defined below), so the optimal plan is to consume everything:

(12)

Now define nonbold variables as the bold variable divided by the

level of permanent income in the same period, so that, for example,

; and define

.3

For our CRRA utility function, ,

so (12) can be rewritten as

(13)

Because we are dividing

level variables by ,

a normalized return factor emerges:

(14)

(We treat

as time-invariant and drop the period subscript that appeared in (3).)

Now define a new optimization problem:

(15)

(16)

Then it is easy to see that for , we

can write boldface (nonnormalized)

as a function of

(normalized value) and permanent income:

(17)

and so on back to all earlier periods (by backward induction: if the factorization holds at

, substituting into the

Bellman equation at

and using the homogeneity of CRRA utility yields the same factorization at

).

Hence, if we solve the problem (16) which has only a single state variable

, we can

obtain the levels of the value function from (17), and of consumption and all other variables

from the corresponding permanent-income-normalized solution objects by multiplying each by

,

e.g.

We have thus reduced the problem from two continuous state variables to one (and thereby enormously

simplified its solution).4

For future reference it will be useful to write (16) in the traditional way, by substituting

and

into

:

(18)

4 Notation

4.1 Periods, ,

The problem so far assumes that the agent has only one decision. But agents often have multiple

choices per period—for example, a consumption decision, a labor supply choice, and a choice of what

proportion

of capital

to invest in a risky vehicle. We identify each type in two ways: by a short-name (a textual

name, given when the stage is first introduced) and by a control-name (the stage’s control

variable, if any). For example, a labor supply might have short-name labor and control-name

; a consumption

has control-name .

A stage list that constitutes a period may therefore be written by short-name,

e.g. , or by

control-name, e.g. .

A modeler might want to explore whether the order in which the are solved makes any

difference, either to the substantive results or to aspects of the computational solution like

speed and accuracy; with this scheme they do so merely by changing the order in which the

stages are listed in the specification of the period.

If, as in section 2, we hard-wire into the solution code for each an assumption that its

successor will be something in particular (say, the consumption assumes that the portfolio

choice is next), then if we want to change the order of the (say, labor supply after

consumption, followed by portfolio choice), we will need to re-hard-wire each of the stages to

know new things about its new successor (for example, the specifics of the distribution of the

rate of return on the risky asset must be known by whatever precedes the portfolio choice

).

The cardinal insight of ? is that everything that matters for the solution to the current

problem is encoded in a ‘continuation-value function.’

Using that insight, we describe here a framework for isolating the problems within a period

from each other, and the period from its successors or predecessors in any other period. The

advantage of this isolation is that each problem becomes a self-contained module: Its internal

logic—the computation it performs on value functions—is defined independently of where it

sits in the sequence of .

Modularity is valuable because it makes exploring such alternative model

structures cheap. Using control-name indexing (e.g., the consumption by

), after considering

the -order ,

the modeler can reorder the to consider, say, the order

without rewriting any of the code that solves each individual

.5

What must change are the transitions—the mappings that connect the end of one to the

beginning of the next—which must be rewired to reflect the new ordering and its implied

information structure. The -level code itself remains untouched.

4.2

The key is to distinguish, within each ’s Bellman problem, three viewpoints or ‘’ (we use that

word to empasize that the does not do anything: It is merely a collection of mathematical and

computational functions and objects).

: Incoming state variables (e.g., )

are known, but any shocks associated with the have not been realized and

decision(s) have not yet been made

: The agent solves the decision problem for the period

: After all decisions have been made, their consequences are measured by evaluation

of the continuing-value function at the values of the ‘outgoing’ state variables

(sometimes called ‘post-state’ variables)

This framework is deliberately silent about when shocks (if any) occur within a . Shocks may be

realized between the and , or between the and —the choice is part of the ’s specification,

not a framework-level constraint. In a consumption problem, the usual assumption is that

income shocks have been realized before the spending decision is made, so that the consumer

knows their resources when they decide how much to spend; here, shocks fall between and

().

But in a portfolio choice problem, the portfolio share decision must be

made before the return shock is realized; there, shocks fall between and

().

The structure accommodates both patterns: the -to- relationship encodes

pre-decision uncertainty, while the -to- relationship encodes post-decision

uncertainty. A with no shocks at all (such as cons-noshocks or disc) simply sets

or

with

no intervening expectation.

Table 1: within the cons-with-shocks

Indicator

State

value functions

Explanation

value at entry to

(s)

value of -decision

value at exit

This cons-with-shocks corresponds to the consumption problem defined above.

The table illustrates notation we can use when analyzing the problem from

a context ‘inside’ a particular stage of a specific period. We require that no

variable can have more than one meaning or interpretation inside a period, and

we prohibit any reference to values of any variables or functions or other model

objects from outside the stage (or period). This is why we use different letters,

and

, to represent liquid

resources before and after the consumption decision, even if ultimately this period’s continuation value of

will transmute into the

next period’s initial .

(Both

and are

“k-type” variables—investable capital before returns are realized; the distinction from “m-type”

variables like ,

which represent spendable resources after returns, is formalized below.)

In contrast, items like value functions

or expectations operators

have different meanings at different perches; we capture this using a subscript like

.

The fact that all functions in a perch depend on the same state variables (shown

in the second column) allows us to write those functions without specifying their

arguments.

4.3 Builders and Connectors

Modularity requires that objects inside a period have no direct access to

objects from any other period. This means that we must endow a or a

period, at the time of its creation, with its end-of–or-period value function

.

For example, in a model in which every period contains only the single-stage consumption

problem above, the continuation value function for the last (and only) stage at will need to be

’connected’ to the arrival value function in (+1), which of necessity requires us to use

-related notation. Concretely, if we designate the end-of-period value function as

(which

is defined as the continuation value function from the last in the period), we use the notation

(19)

to describe what the builder does when constructing the predecessor to period

. The use

of the ‘’

signals creation: the left-hand side is brought into existence by the builder.

Expectation operators across .

The subscript on an expectation operator

indicates the

information set at that :

conditions on the state but not on any shocks realized between and . For adjacent at a period

boundary—

( of period )

and ( of

period )—the

information sets are identical, so the two operators are mathematically

interchangeable; the notational distinction reflects viewpoint (looking backward from

’s exit versus

forward from ’s

entry).

Tying two adjacent or periods together also requires that we define a ,

, which

specifies the relationship between the continuation-perch state variable(s) of the predecessor to

the arrival-perch state variable(s) of the successor. Again concretely, for two successive periods

each of which contains only a single consumption like the one described above, the would

look like:

(20)

State-variable types.

Every state variable in the framework belongs to exactly one of two types:

k-type (capital): investable assets before returns and income are realized.

The defining characteristic is that a k-type variable must pass through a

returns-and-shocks process before it becomes spendable. Examples:

(beginning-of-period capital) and

(end-of-period assets after consumption, awaiting next period’s returns).

m-type (market resources): spendable resources after returns and income shocks

have been realized—what ? calls “cash-on-hand.” The defining characteristic is that

an m-type variable is immediately available for spending or allocation decisions.

Examples:

(market resources at the ) and

(post-shock market resources within a period).

Well-typed connectors. A is a pure rename: it asserts that two variables from adjacent or

periods are different names for the same economic object. A is well-typed if and only if the

two variables it connects share the same type. Thus:

is well-typed: both are k-type.

is well-typed: both are m-type.

would be illegal:

is m-type and

is k-type. Market resources and investable capital are not merely different

names for the same quantity—converting between them requires a substantive

transformation (the realization of returns and income). Attempting such a

connector is a modeling error: it would silently skip the returns process, treating

post-return resources as if they were pre-return capital.

The type constraint prevents a common class of modeling errors in which a modeler

inadvertently connects a post-return variable to a pre-return slot (or vice versa), producing

economically nonsensical dynamics. By requiring type agreement, the framework ensures that

every transition between k-type and m-type passes through an explicit returns-and-shocks

.

Annotating stage tables with types.

When reading the tables in this document and in section 9, the arrival and continuation

state types can be read off directly:

disc: arrival and continuation inherit the type of the predecessor’s exit state

(passthrough).

A within-period between two must respect the same type constraint: the predecessor ’s

continuation type must match the successor ’s arrival type.

Namespace uniqueness and the decoration.

A strict rule of the framework is that each variable name refers to exactly one valuewithin a given period. This namespace uniqueness constraint ensures that the mapping

between mathematical symbols and computational variables (e.g., Python names) is

well-defined: if a symbol appears in an equation, there is no ambiguity about which quantity it

denotes.

The constraint has a practical consequence when multiple within the same period

produce variables of the same type. For example, in the portable–consnoshocks

period (section 9.2.5.0), the portable produces post-shock market resources, and the

cons-noshocks receives market resources as its state. Both quantities are m-type, but

they arise at different points in the period and generally take different values. To

preserve namespace uniqueness, the earlier occurrence receives a decoration: we write

for the portable ’s output

and for the cons-noshocks

’s input. The within-period

then renames one to the other.

More generally, when a ’s continuation state has the same type as another ’s arrival state

within the same period, the later or secondary occurrence may receive a decoration

(,

, etc.)

to maintain uniqueness. The decoration signals that the variable is of the same economic type

as its undecorated counterpart but occupies a distinct position in the period’s computation.

This convention makes it straightforward to translate the mathematical notation into code:

each decorated symbol maps to a unique Python variable name (e.g., mNrmCheck for

, mNrm

for ),

and no variable is overwritten or reused within a single period’s scope.

4.4 The Pile: Definition and Construction

4.4.1 Formal Definition

The pile

is an ordered sequence of solved periods interleaved with the that join them. Formally, a pile

with

periods is:

(21)

where each

is a solved period (containing its stage list, value functions, and policy functions) and each

is a

between-period satisfying the type constraint from section 4.3: the predecessor’s exit state

and the successor’s entry state must share the same type (k-type or m-type).

The pile is well-formed if and only if every adjacent

triple

satisfies:

Type consistency. The continuation-state type of ’s

last matches the arrival-state type of ’s

first , and the is a valid rename between them.

Value-function compatibility. The and builder together produce a

continuation value function for

from the arrival value function of .

4.4.2 The Consumption-Only Pile

For the consumption-only problem of sections 2–3, each period contains the stage list

(or, in the single-

formulation, just ).

The between-period is

(both k-type). A three-period consumption-only pile is therefore:

4.4.3 Homogeneous and Heterogeneous Piles

A pile is homogeneous if every period has the same stage list, the same parameter values, and

the same between-period . The infinite-horizon consumption problem (section 7) converges to a

homogeneous pile: every period is identical, and the converged solution is a fixed point of the backward

builder .

A pile is heterogeneous if periods differ in their stage lists, parameter values, or . A life cycle

model is typically heterogeneous: mortality risk, income profiles, and available choices (e.g.,

whether portfolio optimization is active) may vary by age. For example, a life cycle model might

use

for working-age periods (with active portfolio choice) and

for

retirement periods (no portfolio choice).

4.4.4 Backward Construction

We call the structure in which accumulating periods are stored the pile

.

Once backward induction is complete, the pile holds the full definition of the solved

problem.

The process of building the pile is straightforward. We start from the terminal period (section 3:

, consume everything),

so initially . We denote

the backward builder as .

Applying to

the existing

creates a new and then the new period’s solution, yielding

. Each subsequent

application of

prepends one more

pair, growing the pile from right to left. Section 6 details the construction of

; with

multiple or control variables the structure generalizes as in section 9.

5 The Usual Theory, and a Bit More Notation

For reference and to illustrate our new notation, we will now derive the Euler

equation and other standard results for the problem described above. Since

we can write value as of the end of the consumption stage as a function of

:

(22)

Derivative notation convention.

Throughout this document, a

superscript

on a function means its derivative with respect to the relevant state variable at that perch:

,

.

So, the first order condition for (18) with respect to

6

is

(23)

which illustrates the derivative convention

(e.g. is the derivative

of with respect

to its argument).7

For functions of more than one argument, we append the variable name:

denotes the partial

derivative of

with respect to .

we can substitute the LHS of (24) for the RHS of (23) to get

(25)

(26)

and rolling forward one period,

(27)

so that substituting the LHS in equation (23) finally gives us the Euler equation for

consumption:

(28)

(29)

The derivation above used period-qualified subscripts (e.g.,

,

)

because the Euler equation relates objects across periods. We can now restate the

problem (18) using the simpler within- notation, which drops the period qualifier:

(30)

whose first order condition with respect to

is

(31)

which is mathematically equivalent to the usual Euler equation for consumption.

We will revert to this formulation when we reach subsection 6.9.

6 Solving the Next-to-Last Period

This section examines the second-to-last period in detail, illustrating a number of powerful

techniques for speeding and improving its solution; in doing so it illustrates how the pile

(subsection 4.4) is

built backward. We set

here to reduce clutter.

6.1 A Direct Expression for

If , the

second-to-last-period decision-perch problem is

(32)

Using (0) ;

(1) ; (2) the

definition of ;

and (3) the definition of the expectations operator,

(33)

where is the cumulative

distribution function for ,

this maximization problem implicitly defines a ‘period-and–local function’

that yields optimal consumption

in period for any specific

numerical level of resources like .

The explicit statement of the problem is

(34)

But because there is no general analytical solution, for any given

we must use numerical

tools to find the

that maximizes the expression. This is excruciatingly slow: for every candidate

, a definite

integral over

must be calculated numerically, and optimization is itself a costly operation, so the

combination of the two is a double-whammy for slowdown.

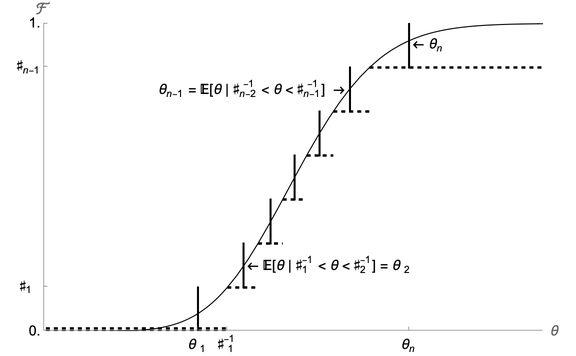

6.2 Discretizing the Distribution

Our first speedup trick is therefore to construct a discrete approximation to the lognormal distribution

that can be used in place of numerical integration. That is, we want to approximate the expectation over

of a function

by calculating its

value at set of points

, each of which has an

associated probability weight :

(because adding

weighted values to each other is enormously faster than general-purpose numerical

integration).

Such a procedure is called a ‘quadrature’ method of integration; ? survey

a number of options, but for our purposes we choose the one which is easiest to

understand: An ‘equiprobable’ approximation (that is, one where each of the values of

has an equal

probability, equal to ).

We calculate such an -point

approximation as follows.

Define a set of points from

to on the

interval as the elements of the set

.8

Call the inverse of the

distribution , and define the

points . Then the conditional

mean of in each of the

intervals numbered 1 to

is:

(35)

and when the integral is evaluated numerically for each

the result is a set of values

of that correspond to the

mean value in each of the

intervals.

The method is illustrated in Figure 2. The solid continuous curve represents the “true” CDF

for a lognormal

distribution such that ,

. The short vertical line segments

represent the equiprobable

values of which are used to

approximate this distribution.9

Figure 1: Equiprobable Discrete Approximation to Lognormal Distribution

Figure 2: Equiprobable Discrete Approximation to Lognormal Distribution

The following notebook snippet constructs these points.

(36)

We now substitute our approximation (37) for

in (32) which is

simply the sum of

numbers and is therefore easy to calculate (compared to the full-fledged numerical integration

(33)

that it replaces).

(37)

6.3 The Approximate Consumption and Value Functions

Given any particular value of ,

a numerical maximization tool can now find the

that

solves (32) in a reasonable amount of time.

The notebook responsible for computing an estimated consumption function begins in “Solving

the Model by Value Function Maximization,” where a vector of possible values of market resources

is created. In these

notes we use for

such a vector (e.g.

the first entry,

the last). For illustration we take the grid to be the first five nonnegative integers,

.

6.4 An Interpolated Consumption Function

This is accomplished in “An Interpolated Consumption Function,” which generates an interpolating function

that we designate .

Figures 3 and 4 show plots of the constructed

and

. While the

function looks very

smooth, the fact that the

function is a set of line segments is very evident. This figure provides the beginning of the

intuition for why trying to approximate the value function directly is a bad idea (in this

context).10

Figure 3:

(solid) versus

(dashed)

Figure 4:

(solid) versus

(dashed)

6.5 Interpolating Expectations

Piecewise linear ‘spline’ interpolation as described above works well for generating a

good approximation to the true optimal consumption function. However, there is

a clear inefficiency in the program: Since it uses equation (32), for every value of

the program must calculate the utility consequences of various possible choices of

(and

therefore )

as it searches for the best choice.

For any given index

in , as it searches for the

corresponding optimal , the

algorithm will end up calculating

for many values close to the

optimal . Indeed, even when

searching for the optimal

for a different

(say for

) the search process

might compute

for an close to the

correct optimal

for .

But if that difficult computation does not correspond to the exact solution to the

problem, it is discarded.

The notebook section “Interpolating Expectations,” now interpolates

the expected value of ending the period with a given amount of

assets.11

Figure 5 compares the true value function to the approximation produced by following the

interpolation procedure; the approximated and exact functions are of course identical at the

gridpoints of

and they appear reasonably close except in the region below

.

Figure 5: End-Of-Period Value

(solid) versus

(dashed)

Figure 6:

(solid) versus

(dashed)

Nevertheless, the consumption rule obtained when the approximating

is used

instead of

is surprisingly bad, as shown in figure 6. For example, when

goes from 2 to 3,

goes from about 1 to

about 2, yet when

goes from 3 to 4,

goes from about 2 to about 2.05. The function fails even to be concave, which is distressing

because Carroll and Kimball (?) prove that the correct consumption function is strictly

concave in a wide class of problems that includes this one.

6.6 Value Function versus First Order Condition

Loosely speaking, our difficulty reflects the fact that the consumption choice is

governed by the marginal value function, not by the level of the value function

(which is the object that we approximated). To understand this point, recall

that a quadratic utility function exhibits risk aversion because with a stochastic

,

(38)

(where

is the ‘bliss point’ which is assumed always to exceed feasible

).

However, unlike the CRRA utility function, with quadratic utility the consumption/saving

behavior of consumers is unaffected by risk since behavior is determined by the first order

condition, which depends on marginal utility, and when utility is quadratic, marginal utility is

unaffected by risk:

(39)

Intuitively, if one’s goal is to accurately capture choices that are governed by marginal

value, numerical techniques that approximate the marginal value function will yield a more

accurate approximation to optimal behavior than techniques that approximate the level of the

value function.

The first order condition of the maximization problem in period

is:

(40)

(41)

Figure 7:

versus

The downward-sloping curve in Figure 7 shows the value of

for our baseline

parameter values for

(the horizontal axis). The solid upward-sloping curve shows the value of the RHS of (41) as a function of

under the assumption

that . Optimal

consumption given is the

at which the two curves

intersect—just below . The

dashed curve shows the same for ;

its intersection with

is slightly below ,

so increasing

from 3 to 4 raises optimal consumption by about 0.5.

Now consider the derivative of .

Because the function is piecewise linear, its derivative

is a

step function: constant between adjacent gridpoints, with jumps at each gridpoint.

The solid-line step function in Figure 7 depicts the actual value of

. When we attempt to

find optimal values of

given using

, the numerical optimization

routine will return the

for which . Thus, for

the program will return

the value of for which

the downward-sloping

curve intersects with the ;

as the diagram shows, this value is exactly equal to 2. Similarly, if we ask the routine to find the

optimal for

, it finds the point

of intersection of

with ;

and as the diagram shows, this intersection is only slightly above 2. Hence, this figure

illustrates why the numerical consumption function plotted earlier returned values very close

to for

both

and .

We would obviously obtain much better estimates of the point of intersection between

and

if our

estimate of

were not a step function. In fact, we already know how to construct linear interpolations to

functions, so the obvious next step is to construct a linear interpolating approximation to

the expected marginal value of end-of-period assets function at the points in

:

(42)

yielding (the vector of expected

end-of-period- marginal values

of assets corresponding to ),

and construct

as the linear interpolating function that fits this set of points.

Figure 8:

versus

The results are shown in Figure 8. The linear interpolating approximation looks roughly as

good (or bad) for the marginal value function as it was for the level of the value function.

However, Figure 9 shows that the new consumption function (long dashes) is a

considerably better approximation of the true consumption function (solid) than was the

consumption function obtained by approximating the level of the value function (short

dashes).

Figure 9:

(solid) Versus Two Methods for Constructing

6.7 Transformation

Even the new-and-improved consumption function diverges notably from the true solution, especially at

lower values of .

That is because the linear interpolation does an increasingly poor job of capturing the nonlinearity of

at lower and

lower levels of .

This is where we unveil our next trick. To understand the logic, start by considering the case

where

and there is no uncertainty (that is, we know for sure that income next period will be

).

The final Euler equation (recall that we are still assuming that

) is

then:

(43)

In the case we are now considering with no uncertainty and no liquidity constraints, the optimizing

consumer does not care whether a unit of income is scheduled to be received in the future period

or the

current period ;

there is perfect certainty that the income will be received, so the consumer treats its PDV as

equivalent to a unit of current wealth. Total resources available at the point when the

consumption decision is made is therefore comprised of two types: current market resources

and ‘human wealth’ (the

PDV of future income) of

(because it is the value of human wealth as of the end of the period, there is only one more

period of income of 1 left).

(44)

Of course, this is a highly nonlinear function. However, if we raise both sides of (44) to the

power

the result is a linear function:

(45)

This is a specific example of a general phenomenon: A theoretical literature discussed in ?

establishes that under perfect certainty, if the period-by-period marginal utility function is of the form

, the marginal value

function will be of the form

for some constants .

This means that if we were solving the perfect foresight problem numerically, we could always

calculate a numerically exact (because linear) interpolation.

The key insight is that much of the nonlinearity in

comes from raising to the

power . By inverting that

operation (raising to ),

we can ‘unwind’ it, and the remaining nonlinearity is much smaller.

Specifically, applying the foregoing insights to the end-of-period value function

, we

can define an ‘inverse marginal value’ function

(46)

which would be linear in the perfect foresight

case.12

We then construct a piecewise-linear interpolating approximation to the

function,

, and for any

that falls in

the range

we obtain our approximation of marginal value from:

(47)

The most interesting thing about all of this, though, is that the

function has another interpretation. Recall our point in (31) that

. Since with

CRRA utility ,

this can be rewritten and inverted

(48)

This gives a concrete

interpretation: for any ending ,

it reveals how much the agent must have consumed to (optimally) reach that

. We

will therefore henceforth refer to it as the ‘consumed function:’

(49)

Thus, for example, for period our

procedure is to calculate the vector of

points on the consumed function:

(50)

with the idea that we will construct an approximation of the consumed function

as the interpolating

function connecting these

points.

6.8 The Natural Borrowing Constraint and the

Lower

Bound

This is the appropriate moment to ask an awkward question: How

should an interpolated, approximated ‘consumed’ function like

be extrapolated to return an estimated ‘consumed’ amount when evaluated at an

outside the range

spanned by ?

For most canned piecewise-linear interpolation tools like scipy.interpolate, when the

‘interpolating’ function is evaluated at a point outside the provided range, the algorithm

extrapolates under the assumption that the slope of the function remains constant beyond its

measured boundaries (that is, the slope is assumed to be equal to the slope of nearest

piecewise segment within the interpolated range); for example, if the bottommost gridpoint is

and the corresponding

consumed level is

we could calculate the ‘marginal propensity to have consumed’

and construct the approximation as the linear extrapolation below

from:

(51)

To see that this will lead us into difficulties, consider what happens to the true (not approximated)

as

approaches a quantity we will call the ‘natural borrowing constraint’:

. From

(42)

we have

(52)

But since , exactly at

the first term in the summation

would be which is infinity.

The reason is simple: is the

PDV, as of , of the minimumpossible realization of income in

().

Thus, if the consumer borrows an amount greater than or equal to

(that is, if the

consumer ends

with )

and then draws the worst possible income shock in period

, they will have to

consume zero in period ,

which yields

utility and

marginal utility.

As ? first noticed, this means that the consumer faces a ‘self-imposed’

(or, as above, ‘natural’) borrowing constraint (which springs from the

precautionary motive): They will never borrow an amount greater than or equal to

(that is, assets will never

reach the lower bound of ).

The constraint is ‘self-imposed’ in the precise sense that if the utility function were different

(say, Constant Absolute Risk Aversion), the consumer might be willing to borrow more than

because a choice of zero or negative consumption in period

would yield some finite

amount of utility.13

This self-imposed constraint cannot be captured well when the

function is approximated by a piecewise linear function like

,

because it is impossible for the linear extrapolation below

to correctly

predict

So, the marginal value of saving approaches infinity as

. But this

implies that ;

that is, as

approaches its ‘natural borrowing constraint’ minimum possible value, the corresponding amount of

worst-case

must approach its lower bound: zero.

The upshot is a realization that all we need to do to address these problems is to prepend each

of the and

from (50)

with an extra point so that the first element in the mapping that produces our interpolation

function is .

This is done in section “The Self-Imposed ‘Natural’ Borrowing Constraint and the

Lower

Bound” of the notebook.

Figure 10: True

vs its approximation

Figure 10 shows the result. The solid line calculates the exact numerical value of the consumed

function

while the dashed line is the linear interpolating approximation

This

figure illustrates the value of the transformation: The true function is close to linear, and so the

linear approximation is almost indistinguishable from the true function except at the very lowest

values of .

Figure 11 similarly shows that when we generate

using our

augmented

(dashed line) we obtain a much closer approximation to the true marginal value function

(solid

line) than we obtained in the previous exercise which did not do the transformation

(Figure 8).

Figure 11: True

vs.

Constructed Using

6.9 The Method of Endogenous Gridpoints (‘EGM’)

The solution procedure above for finding

still requires us, for each point in ,

to use a numerical rootfinding algorithm to search for the value of

that

solves .

Though sections 6.7 and 6.8 developed a highly efficient and accurate procedure to calculate

, those

approximations do nothing to eliminate the need for using a rootfinding operation for calculating, for

an arbitrary ,

the optimal .

And rootfinding is a notoriously computation-intensive (that is, slow!) operation.

Fortunately, it turns out that there is a way to completely skip this slow rootfinding step. The

method can be understood by noting that we have already calculated, for a set of arbitrary values of

, the corresponding

values for

which this

is optimal.

But with mutually consistent values of

and (consistent,

in the sense that they are the unique optimal values that correspond to the solution to the problem), we

can obtain the

vector that corresponds to both of them from

(53)

These gridpoints

are “endogenous” in contrast to the usual solution method of specifying some ex-ante (exogenous) grid

of values of

and then using a rootfinding routine to locate the corresponding optimal consumption vector

.

This routine is performed in the “Endogenous Gridpoints” section of the notebook. First, the

endOfPrd.cCntn_Tm1 function is called for each of the pre-specified values of end-of-period assets

stored in .

These values of consumption and assets are used to produce the list

of endogenous gridpoints, stored in the object mVec_egm. With the

values in hand, the notebook

can generate a set of

and

pairs that can be interpolated between in order to yield

at virtually zero

computational cost!14

One might worry about whether the

points obtained in this way will provide a good representation of the consumption function as

a whole, but in practice there are good reasons why they work well (basically, this procedure

generates a set of gridpoints that is naturally dense right around the parts of the function with

the greatest nonlinearity).

Figure 12:

(solid) versus

(dashed)

Figure 12 plots the actual consumption function

and the approximated

consumption function

derived by the method of endogenous grid points. Compared to the approximate consumption functions

illustrated in Figure 9,

is quite close to the actual consumption function.

6.10 Improving the

Grid

Thus far, we have arbitrarily used

gridpoints of (augmented

in the last subsection by ).

But it has been obvious from the figures that the approximated

function tends to be farthest from its true value at low values of

. Combining this

with our insight that

is a lower bound, we are now in position to define a more deliberate method for constructing

gridpoints for

– a method that yields values that are more densely spaced at low values of

where

the function is more nonlinear.

A pragmatic choice that works well is to find the values such

that (1) the last value exceeds the lower bound by the same amount

as

our original maximum gridpoint (in our case, 4.); (2) we have the same number

of gridpoints as before; and (3) the multi-exponential growth rate (that is,

for some number

of exponentiations

– our default is 3) from each point to the next point is constant (instead of, as previously,

imposing constancy of the absolute gap between points).

Figure 13:

versus ,

Multi-Exponential

Figure 14:

vs. ,

Multi-Exponential

Section “Improve the ”

begins by defining a function which takes as arguments the specifications of an initial grid of

assets and returns the new grid incorporating the multi-exponential approach outlined

above.

Notice that the graphs depicted in Figures 13 and 14 are notably closer to their respective

truths than the corresponding figures that used the original grid.

6.11 Program Structure

In section “Solve for

in Multiple Periods,” the natural and artificial borrowing constraints are combined with the

endogenous gridpoints method to approximate the optimal consumption function for a

specific period. Then, this function is used to compute the approximated consumption

in the previous period, and this process is repeated for some specified number of

periods.

The essential structure of the program is a loop that iteratively solves for consumption

functions by working backward from an assumed final period, using the dictionary

cFunc_life to store the interpolated consumption functions up to the beginning period.

Consumption in a given period is utilized to determine the endogenous gridpoints for the

preceding period. This is the sense in which the computation of optimal consumption is done

recursively.

In the terminology of section 4.3, each iteration of this backward loop is an invocation of the backward

builder : it creates

the (inserted into

between the new and existing period solutions), uses it and the already-solved next period to perform the

creation of , and

solves for the optimal consumption rule. The dictionary cFunc_life is the computational embodiment

of —the

growing structure of solved periods and between them assembled by backward

induction.

For a realistic life cycle problem, it would also be necessary at a minimum to calibrate a

nonconstant path of expected income growth over the lifetime that matches the

empirical profile; allowing for such a calibration is the reason we have included the

vector

in our computational specification of the problem.

6.12 Results

The code creates the relevant

functions for any period in the horizon, at the given values of

. Figure 15

shows

for . At

least one feature of this figure is encouraging: the consumption functions converge as the

horizon extends, something that ? shows must be true under certain parametric conditions

that are satisfied by the baseline parameter values being used here.

Figure 15: Converging

Functions as

Increases

The construction of

in this single- case uses the builders and connectors of subsection 4.3.

7 The Infinite Horizon

All of the solution methods presented so far have involved period-by-period iteration from an

assumed last period of life, as is appropriate for life cycle problems. However, if the parameter

values for the problem satisfy certain conditions (detailed in ?), the consumption rules (and

the rest of the problem) will converge to a fixed rule as the horizon (remaining lifetime) gets

large, as illustrated in Figure 15. Furthermore, Deaton (?), Carroll (??) and others have

argued that the ‘buffer-stock’ saving behavior that emerges under some further restrictions on

parameter values is a good approximation of the behavior of typical consumers over much of

the lifetime. Methods for finding the converged functions are therefore of interest, and are

dealt with in this section.

Of course, the simplest such method is to solve the problem as specified above for a large

number of periods. This is feasible, but there are much faster methods.

7.1 Convergence

In solving an infinite-horizon problem, it is necessary to have some metric that determines

when to stop because a solution that is ‘good enough’ has been found.

A natural metric is defined by the unique ‘target’ level of wealth that ?

proves will exist in problems of this kind under certain conditions: The

such

that

(54)

where the accent is meant to signify that this is the value that other

’s

‘point to.’

Given a consumption rule

it is straightforward to find the corresponding

. So for

our problem, a solution is declared to have converged if the following criterion is met:

, where

is a

very small number and defines our degree of convergence tolerance.

Similar criteria can obviously be specified for other problems. However, it is always wise to

plot successive function differences and to experiment a bit with convergence criteria to verify

that the function has converged for all practical purposes.

8 The Method of Moderation

The endogenous gridpoints method constructs a consumption function

by interpolating

a finite set of

pairs. A practical problem arises when the approximation must be evaluated at values of

outside the grid: naïve linear extrapolation can predict consumption so high that

precautionary saving turns negative, an economically impossible result.

A solution, developed in ?, exploits the fact that the true consumption function is bounded

between two analytically computable perfect-foresight rules.

Optimist. An agent who is certain that future income shocks will always equal their mean has human

wealth

and consumes

(55)

where

is the minimal marginal propensity to consume of the corresponding perfect-foresight

problem.

Pessimist. An agent who assumes the worst possible income realisation in every future

period has lower human wealth and a consumption floor at

(56)

where

is the natural borrowing constraint.

Realist. The true solution satisfies

for all .

Because the realist’s consumption always lies between these bounds, one can define a

moderation ratio

(57)

which measures how close the realist is to the optimist

() versus the pessimist

(). The key insight is that

the logit of this ratio, ,

is nearly linear in

and therefore easy to interpolate accurately. Consumption is recovered via the inverse

transformation:

(58)

where

is the logit-transformed moderation ratio. Since the recovered

is

automatically sandwiched between the bounds, the extrapolation problem vanishes.

Figure 17 illustrates the idea: the realist consumption function (middle curve) is bounded

above by the optimist and below by the pessimist.

Figure 16: Moderation Illustrated:

Figure 17: Moderation Illustrated:

The full treatment in ? extends the method with tighter upper bounds, applies an analogous

transformation to the value function, and shows how to handle stochastic returns and Hermite

interpolation refinements.

9 Multiple Control Variables and Modularity

We now consider problems with multiple control variables. Section 9.1 presents the

joint consumption-and-portfolio optimization as a canonical example: we derive the

simultaneous first-order conditions and show that direct numerical solution of the

multidimensional problem is computationally expensive—but that decomposing it

into a sequence of single-control problems is much faster. Section 9.2 develops the

stage-based machinery for such decompositions, building on the modular notation from

section 4: the discounting (disc), the standalone portfolio optimization (section 9.2.2),

and the general-purpose portable returns that unifies portfolio choice and shock

realization. Section 9.2.5 combines these building blocks into three canonical period

types.

9.1 The Joint Optimization Problem

Our canonical example of a multi-control problem is the case where the agent has both a consumption choice

and a decision about

(archaic Greek stigma): the share of assets in the risky asset. Given a risky-asset return factor

and a riskless

return factor ,

the realized portfolio return is

(59)

Written as a single combined decision (substituting the budget constraint):

(60)

Whether the stochastic variables

and

are revealed at the end of the current period or the start of the next does not affect this

equation. The first-order conditions for this joint problem are:

(61)

Direct simultaneous solution of these two conditions is computationally expensive; the

remainder of this section develops modular -based machinery that decomposes the problem

into a sequence of simpler single-control optimizations.

9.2 Decomposing Into Modular Stages

The single–per-period formulation from sections 2–6 is equivalent to a sequence of simpler ,

each with a single job. We decompose it in that way so that adding portfolio choice later

requires no change to the consumption- code—only the stage list and the s between change

(see section 4). The decomposition yields the same value functions, consumption function, and

Euler equation.

Stage graphs: from lists to directed acyclic graphs.

The stage lists presented above—e.g.,

—are

linear: each has exactly one predecessor and one successor. More generally, the within a

period may form a directed acyclic graph (DAG), in which a single predecessor fans out

into multiple successor branches that later reconverge. Each branch represents a

distinct contingency or regime that the agent may face, and the value function

of the branching is a probability-weighted combination of the values from the

branches.

Example: employment branches (expository).

Consider a consumer who, at the start of each period, is either employed or temporarily unemployed,

with probabilities

and

respectively. The two labor-market states imply different income processes:

Employed branch. The consumer receives ordinary labor income ,

so market resources are .

Unemployed branch. The consumer receives unemployment insurance benefits

(a fixed fraction of permanent income), so market resources are .

After the branch-specific income is realized, both branches feed into

the same shock-free consumption (cons-noshocks), which chooses

given

. The

DAG for a single period is:

employed-shocks

branch

cons-noshocksdisc

unemployed-shocks

The branching has no optimization; it merely routes the agent into one of the two

income-realization with the appropriate probability. The value function at the branch point

is:

Each branch is itself a valid (with its own , , and ); the only new element is the

probability-weighted fan-out at the branch point and the fan-in (via a shared ) before the

consumption . This example is purely expository—no code implementation is provided—but it

illustrates how the DAG generalization accommodates heterogeneous regimes within a single

period without duplicating the consumption- logic.

9.2.1 The Discounting Stage (disc)

The simplest decomposition isolates discounting into a standalone

that applies for the entire period. We call it the disc (control-name

). From equation (19),

; the factor

was implicitly inside

the backward builder

that created .

Instead, henceforth at the end of every period, we put the stub disc

which has no choice, no shocks, and a trivial decision value function

, and we set

the discount factor to 1 for every prior stage in the period (leaving all the discounting to the disc

stage).15

Table 2: Discounting ()

Indicator

State

value functions

Explanation

no shocks

(s)

apply

value at exit

n.b.:is a generic passthrough state whose type (k-type or m-type) is inherited from the predecessor ’s state. For example, when disc follows cons-noshocks,stands for(k-type); when it follows portable,stands for(m-type).

Table 3: Rosetta Stone: disc Stage Variables

Math Symbol

LaTeX Macro

Python Variable

Description

—

state

Passthrough state (inherits type from predecessor)

\DiscFac

DiscFac

Time-preference discount factor

\vFunc_{\DiscFac,\dcsn}

vDcsn

Decision value: (no optimization)

\vFunc_{\DiscFac,\cntn}

vCntn

Continuation value function (value at exit)

\vFunc_{\DiscFac,\arvl}

vArvl

Arrival value function (; no shocks)

The two- period has stage list

(more compactly, ).

The convention that every non-disc is undiscounted and every period ends with disc will

mean we do not have to rearrange discounting as we rearrange stages within the

period.

9.2.2 The Standalone Portfolio Problem

Consider the standalone problem of an ‘investor’ choosing the portfolio share

. The state variable at the

start is (capital available for

investment); the chooses ;

stochastic shocks (,

) are then realized,

yielding the state .

The portfolio share must be chosen before the return shock

is realized.

We write

rather than

for the post-shock state because a strict rule of our framework is the

prohibition of multiple timings of a given variable within a period. Note that

is m-type (market resources

after shocks), matching ;

the

decoration distinguishes the two timings while preserving the type (see section 4.3).

The first-order condition with respect to

is:

(62)

(63)

where

denotes the derivative of the continuation value function with respect to

.

The equation yields the portfolio share function:

(64)

(65)

9.2.3 The portable Stage

The portfolio optimization problem above can be generalized into a single configurable

returns-and-shocks by making the portfolio share an optional parameter rather than a control

variable that must always be optimized. We call this the portable (“portfolio-able”):

it is “able” to perform portfolio optimization or not, depending on a parameter

.

The ’s state includes the investable capital

and an optional

portfolio share ,

where

means “absent—optimize.” The behavior of the depends on

:

Optimize mode ():

The solves the portfolio optimization problem from section 9.2.2, choosing

optimally via (65) with first-order condition (63).

Fixed-share mode ():

The portfolio share is prescribed; no optimization occurs. The value function is

.

No-risky-investment mode ():

A special case of fixed-share mode. All assets earn the riskless return:

.

The risky return

is irrelevant. The value function reduces to .

The of this are:

Table 4: portable

Indicator

State

value functions

Explanation

no pre-decision shocks

(s)

depends on (see above)

choose or use

post-shock value

Table 5: Rosetta Stone: portable Stage Variables

Math Symbol

LaTeX Macro

Python Variable

Description

\kNrm

kNrm

Normalized capital (arrival state, k-type)

\shr

Shr

Portfolio share in risky asset (control or fixed parameter)

When , the value

function is .

When , it

is with

fixed

at .

Argument notation.

When a stage can be constructed with a fixed parameter, we write the value of that argument in parentheses.

Thus denotes the

portable stage with

(the shocks-only configuration described below), and

denotes portable in optimize mode.

9.2.4 Separating Shocks from Choices

The cons-with-shocks in section 4.2 combines the

shock realization

and the

consumption decision. We split these into two .

The shocks-only stage (portable with).

Calling the portable with

produces a whose only function is to draw the shocks. We call

this configuration shocks-only. It handles the transition from capital

to (post-shock)

market resources :

with , the transition

is —precisely

the

mapping from the original problem (the next stage receives this as

). No

optimization occurs:

Table 6: shocks-only (portable with )

Indicator

State

value functions

Explanation

pre-shock value

(s)

(none)

no choice

post-shock value

The value function takes the expectation over the shocks:

. The

state

is fully determined (non-stochastic) once the shocks are realized.

The shock-free consumption stage (cons-noshocks).

With shocks in the preceding , the consumption has state

and no shocks between

and , so . We call this the

cons-noshocks (control-name ):

The equation for this defines the consumption function:

(66)

(67)

The is unchanged from the single- formulation. But this stage is a ’stub’:

It could not be the only stage in a period because its continuation state

is of a different type

than its arrival state .

A full period would require it to be paired with another stage that produced the transition

from

to .

The three-stage period.

The consumption-only period from sections 2–6 is defined by the stage list

, or equivalently

in control-name

form (recall denotes

portable with ;

see section 9.2.3). Explicitly:

Element

Transition

Action

shocks-only

shocks realize (no choice)

rename

cons-noshocks

choose

disc

apply

This is functionally identical to the single- formulation. Each resolves its stochastic content

internally; the value at a ’s exit is therefore non-stochastic.

Multi-stage notation.

Once our Pile

has accumulated multiple periods and , we address any perch-specific object (like a value

function) by comma-separated subscripts, ordered from outermost to innermost—period, , :

We drop the period when considering a from a context inside a period

().

9.2.5 Three Period Types

Using the portable (with

or ),

the cons-noshocks , and the disc at the end of every period, we can construct three kinds of

periods. A period type is defined by its stage list (section 4), written in square

brackets:

Table 9: Three Period Types

Period type

Transition

Description

shocksonly–consnoshocks

No portfolio choice

portable–consnoshocks

Beginning-of-period returns

consnoshocks–portable

End-of-period returns

We now describe these three variants in detail. We present the consnoshocks–portable

(end-of-period returns) variant first, because it makes the need for the

notation most transparent.

The consnoshocks–portable period (end-of-period returns).

If the portfolio share choice is made and stochastic shocks are realized

at the end of the period, the shock-free consumption comes first and the

follows: stage list

by control-name .

The flow is:

Element

Transition

Action

cons-noshocks

choose

rename

portable

choose , shocks realize

disc

apply

The within-period relabels

the consumption ’s output as the

’s input; the remaining s are catalogued in section 9.2.6. The reason we used

rather

than

for the post-portfolio state now becomes evident: this prevents two different values of

from coexisting within the

same period. The decoration

is appropriate because

remains m-type—it is market resources, differing from

only

in timing.

The portable–consnoshocks period (beginning-of-period returns).

The beginning-returns problem places the

before the shock-free consumption : stage list by control-name

. The

first-order condition for the portfolio-choice is (63).

The flow through a single period is:

Element

Transition

Action

portable

choose , shocks realize

rename

cons-noshocks

choose

disc

apply

Since all stochastic shocks are realized inside the

, the value

that exits it is fully

determined. The within-period

therefore simply relabels

as for

the consumption (see section 9.2.6 for the full catalogue).

The shocksonly–consnoshocks period.

This is the three-stage decomposition from above:

.

A life cycle model in which portfolio choice is available at some ages

but not others is now trivially constructed: the modeler simply sets

for ages with active

portfolio choice and

for ages without.

9.2.6 Connectors for Each Period Type

To construct a Pile

that repeats instances of a given period type, the backward builder

must know the between-period that ties the last of one period to the first of the

next (see section 4.3). Within-period s are already specified in the period tables

above.

period type

Between-period

shocksonly–consnoshocks

portable–consnoshocks

consnoshocks–portable

Each of these s is a pure rename that respects the state-variable type constraint from section 4.3:

and

are both k-type (capital

before returns), while

and

are both m-type (market resources after returns). The connector is determined

by the predecessor’s exit state and the successor’s first-stage arrival state. For

portable–consnoshocks, the period ends after disc (passthrough), so the exit state is

; the next period’s

portable arrives with ,

hence .

For shocksonly–consnoshocks the same logic gives

. For consnoshocks–portable,

the period exits with ;

the relabels it as

for the next period’s cons-noshocks .

9.2.7 Numerical Solution

Following the sequential approach outlined in section 9.1, we solve the portfolio numerically for the

optimal at

a vector of

and construct an approximated optimal portfolio share function

as the interpolating function among the members of the

mapping. Having done this, we calculate a vector of values and marginal values at that grid:

(68)

With the

approximation in hand, we construct our approximation to the consumption function using

exactly the same EGM procedure that we used in solving the problem without a portfolio

choice (see (46)):

(69)

which, following the procedure in subsection 6.9, yields an approximated consumption function

.

9.3 Implementation

Following the discussion from section 9.1, to provide a numerical solution to the problem with

multiple control variables, we must define expressions that capture the expected marginal

value of end-of-period assets with respect to the level of assets and the share invested in risky

assets. This is addressed in “Multiple Control Variables.”

9.4 Results With Multiple Controls

Figure 18 plots the

consumption function generated by the program; qualitatively it does not look much

different from the consumption functions generated by the program without portfolio

choice.

But Figure 19 which plots the optimal portfolio share as a function of the level

of assets, exhibits several interesting features. First, even with a coefficient of

relative risk aversion of 6, an equity premium of only 4 percent, and an annual

standard deviation in equity returns of 15 percent, the optimal choice at values of

less than about 2 is for the agent to invest a proportion 1 (100 percent) of

the portfolio in stocks (instead of the safe bank account with riskless return

).

Second, the proportion of the portfolio kept in stocks is declining in the level of wealth - i.e.,

the poor should hold all of their meager assets in stocks, while the rich should be cautious,

holding more of their wealth in safe bank deposits and less in stocks. This seemingly

bizarre (and highly counterfactual – see ?) prediction reflects the nature of the risks

the consumer faces. Those consumers who are poor in measured financial wealth

will likely derive a high proportion of future consumption from their labor income.

Since by assumption labor income risk is uncorrelated with rate-of-return risk, the

covariance between their future consumption and future stock returns is relatively

low. By contrast, persons with relatively large wealth will be paying for a large

proportion of future consumption out of that wealth, and hence if they invest too much

of it in stocks their consumption will have a high covariance with stock returns.

Consequently, they reduce that correlation by holding some of their wealth in the riskless

form.

Figure 18:

With Portfolio Choice

Figure 19: Portfolio Share in Risky Assets

10 Structural Estimation

This section describes how to use the methods developed above to structurally

estimate a life-cycle consumption model, following closely the work of

?.16

The key idea of structural estimation is to look for the parameter values (for the time

preference rate, relative risk aversion, or other parameters) which lead to the best possible

match between simulated and empirical moments.

10.1 Life Cycle Model

Realistic calibration of a life cycle model needs to take into account a few things that we

omitted from the bare-bones model described above. For example, the whole point of the life

cycle model is that life is finite, so we need to include a realistic treatment of life

expectancy; this is done easily enough, by assuming that utility accrues only if you live,

so effectively the rising mortality rate with age is treated as an extra reason for

discounting the future. Similarly, we may want to capture the demographic evolution of

the household (e.g., arrival and departure of kids). A common way to handle that,

too, is by modifying the discount factor (arrival of a kid might increase the total

utility of the household by, say, 0.2, so if the ‘pure’ rate of time preference were

the

‘household-size-adjusted’ discount factor might be 1.2. We therefore modify the model presented

above to allow age-varying discount factors that capture both mortality and family-size changes

(we just adopt the factors used by ? directly), with the probability of remaining alive between

and

captured

by and

with now

reflecting all the age-varying discount factor adjustments (mortality, family-size, etc). Using

(the Hebrew

cognate of )

for the ‘pure’ time preference factor, the value function for the revised problem is

(70)

(71)

subject to the constraints

where

and all the other variables are defined as in section 2.

Households start life at age and live

with probability 1 until retirement ().

Thereafter the survival probability shrinks every year and agents are dead by

as

assumed by Cagetti.

Transitory and permanent shocks are distributed as follows:

(72)

where

is the probability of unemployment (and unemployment shocks are turned off after

retirement). Transitory and permanent shocks are distributed as follows:

(73)

where

is the probability of unemployment (and unemployment shocks are turned off after

retirement).

The parameter values for the shocks are taken from Carroll (?),

,

, and

.17

The income growth profile is from

Carroll (?) and the values of and

are obtained from Cagetti (?)

(Figure 20).18

The interest

rate is assumed to equal .

The model parameters are included in Table 10.

The structural estimation of the parameters

and

is

carried out using the procedure specified in the following section, which is then implemented

in the StructEstimation.py file. This file consists of two main components. The first section

defines the objects required to execute the structural estimation procedure, while the second

section executes the procedure and various optional experiments with their corresponding

commands. The next section elaborates on the procedure and its accompanying code

implementation in greater detail.

10.2 Estimation

When economists say that they are performing “structural estimation” of a model like this, they

mean that they have devised a formal procedure for searching for values for the parameters

and

at

which some measure of the model’s outcome (like “median wealth by age”) is as close as

possible to an empirical measure of the same thing. Here, we choose to match the

median of the wealth to permanent income ratio across 7 age groups, from age

up to

.19

The choice of matching the medians rather the means is motivated by the fact that the wealth

distribution is much more concentrated at the top than the model is capable of

explaining using a single set of parameter values. This means that in practice one

must pick some portion of the population who one wants to match well; since the

model has little hope of capturing the behavior of Bill Gates, but might conceivably

match the behavior of Homer Simpson, we choose to match medians rather than

means.

As explained in section 3, it is convenient to work with the normalized version of the model

which can be written in Bellman form as:

with the first order condition:

(74)

(75)

The first substantive in this estimation procedure is to solve for the consumption functions

at each age. We need to discretize the shock distribution and solve for the policy functions by

backward induction using equation (75) following the procedure in sections 6 and ‘Recursion.’

The latter routine is slightly complicated by the fact that we are considering a life-cycle model

and therefore the growth rate of permanent income, the probability of death, the time-varying

discount factor and the distribution of shocks will be different across the years. We

thus must ensure that at each backward iteration the right parameter values are

used.

Correspondingly, the first part of the StructEstimation.py file begins by defining the agent

type by inheriting from the baseline agent type IndShockConsumerType, with the modification

to include time-varying discount factors. Next, an instance of this “life-cycle” consumer is

created for the estimation procedure. The number of periods for the life cycle of a given agent